Liposuction is an elective cosmetic procedure and is not covered by health insurance for cosmetic purposes. For most patients, that means paying out-of-pocket — and for a procedure that runs $3,500 to $15,000 depending on body areas and complexity, most patients finance at least part of the cost.

Here is an honest guide to the most common financing options, the interest rates and terms involved, and the deferred interest trap that most patient financing guides quietly omit.

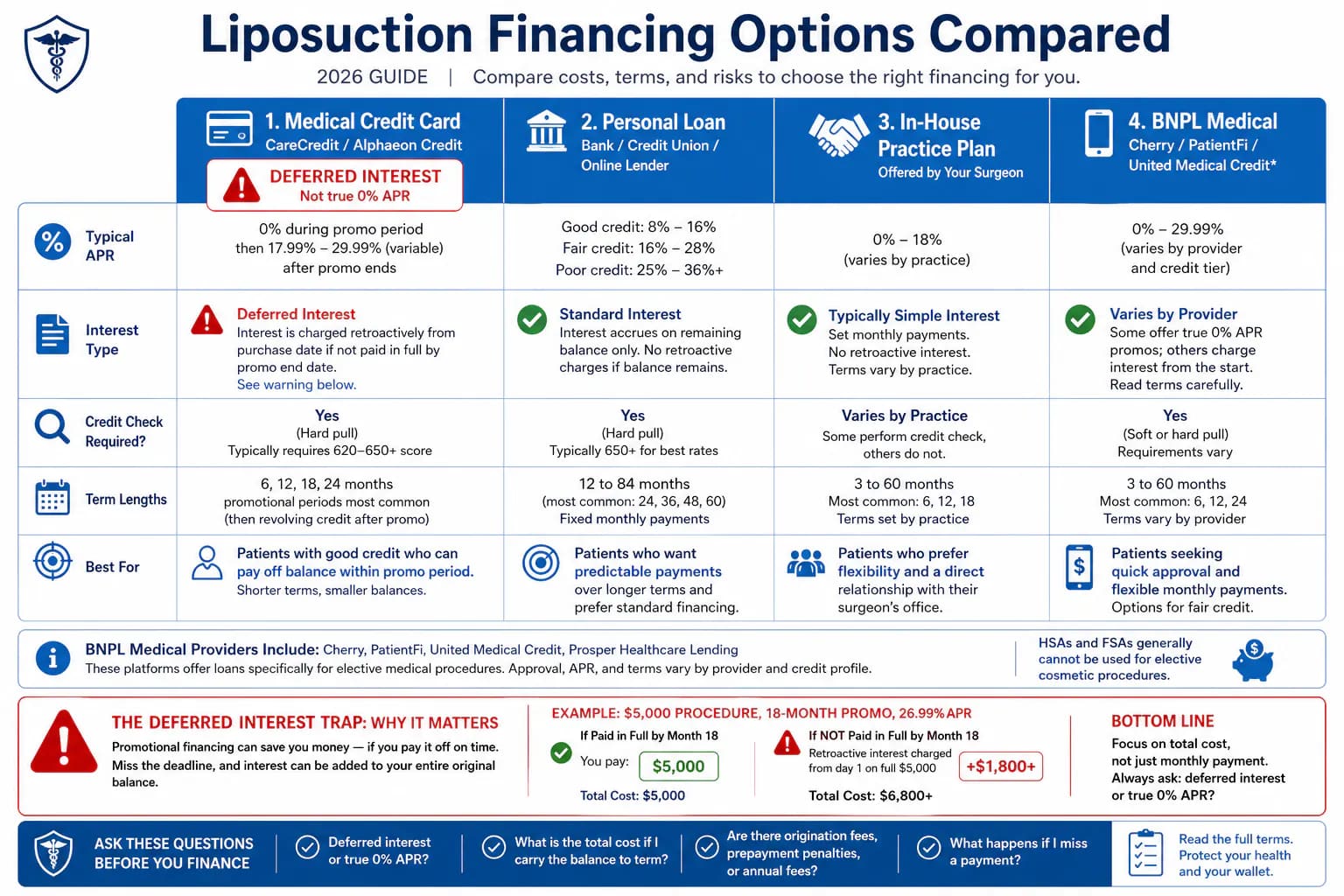

The Main Liposuction Financing Options

1. Medical Credit Cards: CareCredit and Alphaeon Credit

CareCredit is accepted at over 175,000 healthcare providers nationwide and is the most widely used medical financing option for cosmetic surgery. It functions like a credit card dedicated to healthcare expenses.

Key terms:

- Promotional periods of 6, 12, 18, or 24 months with no interest if paid in full by the end date

- After the promotional period, standard APR applies — typically 26.99% to 29.99%

- Accepted at the large majority of plastic surgery practices

Alphaeon Credit is similar to CareCredit, designed specifically for cosmetic and aesthetic procedures:

- Credit lines up to $25,000

- Similar promotional period structure (0% deferred interest for 6–24 months)

- Standard APR after promotional period: 14.90% to 27.99% depending on creditworthiness

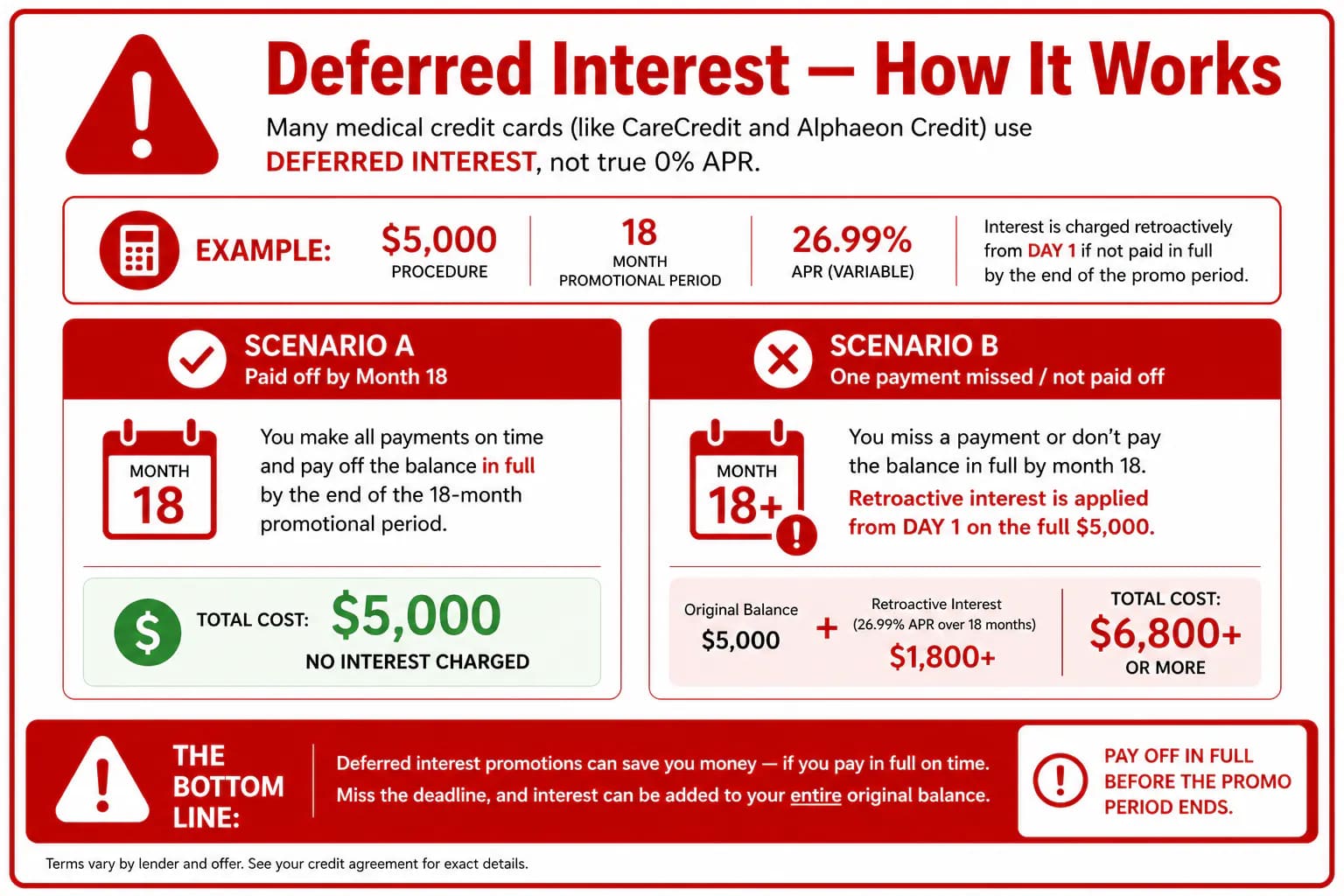

The deferred interest warning — read this carefully:

Both CareCredit and Alphaeon Credit use deferred interest, which is fundamentally different from true 0% APR financing.

With deferred interest:

- Interest accrues on the full balance throughout the promotional period — but it is "deferred" (held back) and not charged unless you fail to pay off the full balance by the promotional period's end date

- If you pay off the balance in full before the deadline: you pay no interest

- If you still have any balance remaining at the promotional deadline — even $1 — the full deferred interest from the entire promotional period is retroactively charged all at once

Example: $6,000 procedure on an 18-month promotional plan at 26.99% APR.

- If paid off by month 18: $6,000 total

- If not paid off by month 18: approximately $2,000+ in retroactive interest is added — making your total cost roughly $8,000 before you've made a single payment toward the principal

This is a significant trap for patients who expect the promotional 0% to work like a conventional 0% APR credit card. It doesn't.

Who this works well for: Patients who can realistically pay off the full balance within the promotional period and are confident they won't miss the deadline.

2. Personal Loans

Personal loans from banks, credit unions, and online lenders are a straightforward alternative to medical credit cards. They use true interest rates, not deferred interest.

Key characteristics:

- Fixed monthly payments over a set term (typically 12 to 60 months)

- APR ranges: 8% to 16% for good credit (670+), 16% to 28% for fair credit (580–669), higher for poor credit

- No retroactive interest surprise — your total cost is calculable upfront

- Not accepted directly by practices — the loan is deposited to your bank account, and you pay the practice

Credit unions typically offer lower rates than banks for personal loans. Online lenders (LightStream, SoFi, Marcus, Discover) compete aggressively on rates for borrowers with good credit.

Who this works well for: Patients who prefer a fixed monthly payment, cannot guarantee they'll pay off a medical credit card within the promotional window, or prefer to know their total cost upfront.

| Credit Score | Typical Personal Loan APR Range |

|---|---|

| 720+ (excellent) | 8% – 12% |

| 670–719 (good) | 12% – 16% |

| 580–669 (fair) | 16% – 24% |

| Below 580 (poor) | 24%+ or secured loan required |

3. Medical Financing Platforms

Several platforms specialize in elective medical procedure financing and serve a wider credit range than traditional lenders:

Cherry: Buy-now-pay-later medical financing. Approves a wide range of credit scores (down to 550+ in some cases). Short-term plans (3, 6, 12 months) and longer plans available. APR varies significantly based on credit tier.

PatientFi: Medical financing platform focused on aesthetic and elective procedures. Works with practices directly. Offers competitive rates for qualified borrowers and more flexible options for lower credit.

United Medical Credit: Serves credit scores as low as 540 in some cases. Multiple lender marketplace — your application is matched with available lenders. Useful if traditional lenders have declined.

Prosper Healthcare Lending: Fixed-rate personal loans specifically for healthcare expenses. True interest rates (no deferred interest). Term options from 24 to 60 months.

4. In-House Practice Payment Plans

Some plastic surgery practices offer their own payment plans — either self-funded or administered through a third party. These vary widely:

- Some practices offer short-term 0% interest plans for 3 to 6 months for patients who pay a deposit

- Others require full payment before surgery

- In-house plans may have less stringent credit requirements

- Terms and penalties for missed payments vary significantly by practice

Ask about in-house financing options during consultation — not all practices advertise them.

True Cost Comparison: What Each Option Costs

For a $6,000 liposuction procedure:

| Financing Option | Term | Rate | Total Cost |

|---|---|---|---|

| CareCredit (paid in full by month 12) | 12 mo promotional | 0% (deferred) | $6,000 |

| CareCredit (balance remaining at month 12) | — | 26.99% retroactive | ~$7,700 |

| Personal loan (good credit) | 36 months | 12% APR | ~$7,113 |

| Personal loan (excellent credit) | 36 months | 9% APR | ~$6,815 |

| Medical platform (fair credit) | 24 months | 20% APR | ~$7,345 |

The difference between "paid off within the promotional period" and "not paid off" on CareCredit can exceed $1,500 on a $6,000 procedure. Calculate whether you can realistically pay off the balance before committing to deferred interest financing.

What Credit Score Do You Need?

| Lender Type | Minimum Credit Score (approximate) |

|---|---|

| CareCredit | 620–650 |

| Alphaeon Credit | 620–650 |

| Personal loan (banks/credit unions) | 650–670 |

| Cherry | 550–580 |

| United Medical Credit | 540+ |

| In-house practice plans | Varies |

Lower credit scores typically result in higher interest rates and shorter promotional periods. Improving your credit score by 30 to 60 points before applying — through on-time payments and debt reduction — meaningfully expands your options.

Questions to Ask Before Signing Any Financing Agreement

1. Is this deferred interest or true 0% APR? If deferred, what is the retroactive rate if I don't pay off in time?

2. What is the total cost if I carry the balance for the full term? Ask for the total interest calculation, not just the monthly payment.

3. Are there prepayment penalties? Some loans charge fees for paying off early.

4. What happens if I miss a payment? Does missing one payment trigger the deferred interest?

5. Is the promotional period 0% from the date of purchase or first use? Some medical credit cards start the clock from card opening, not first use.

Saving vs. Financing: Which Makes More Sense?

If you can save the full amount within 6 to 12 months, paying cash avoids all interest. For a $5,000 procedure, saving $415/month for 12 months gets you there interest-free — compared to $208/month on a promotional credit plan that you'll pay off in 24 months (costing the same amount but over twice as long).

Financing makes sense when:

- Timing matters — a health window, pricing opportunity, or life situation makes surgery appropriate now

- You can qualify for a promotional period and are confident you'll pay it off in time

- The quality-of-life value of the procedure outweighs the cost of borrowing

Can you finance liposuction? Yes — medical credit cards, personal loans, in-house plans, and medical financing platforms all cover liposuction. Insurance does not.

What is the monthly payment? Depends on procedure cost, term, and rate. $5,000 at 0% for 24 months: ~$208/month. $5,000 at 12% APR for 36 months: ~$166/month.

Does CareCredit cover liposuction? Yes — accepted at most practices. But uses deferred interest: if balance isn't paid by the promotional deadline, retroactive interest is charged from day one. Pay it off before the deadline.

What credit score do you need? 620–650 for CareCredit/Alphaeon. 650+ for personal loans at competitive rates. 550+ for some medical financing platforms.

What's the difference between deferred interest and 0% APR? True 0%: no interest accrues during promotional period; post-deadline interest only on remaining balance. Deferred interest: interest accrues silently; if balance remains at deadline, all accumulated interest is charged retroactively. CareCredit uses deferred interest.

Can I get financing with bad credit? Yes — Cherry, United Medical Credit, and some practices serve lower credit scores. Rates and terms are less favorable.

Is it worth financing liposuction? Calculate total cost of borrowing. If you pay off a promotional plan in time: same as cash. If you carry a balance for 3 years at 20%+: the procedure costs significantly more than the quoted price.

Can I use a personal loan? Yes — and for patients who can't guarantee payoff within a promotional period, a personal loan with true fixed interest may be cheaper overall than deferred-interest medical credit cards.

Ready to get quotes from ABPS board-certified surgeons? lipo.com's directory connects you with verified specialists who can provide detailed procedure cost estimates and discuss financing options available through their practice.